The Real Estate Roundtable’s Q1 2024 Sentiment Index confirms that commercial real estate property markets continue to experience significant challenges. At the same time, in the coming year industry executives expect monetary policy action reflecting lower inflation to bring greater stability in asset pricing and expanded availability of debt and equity capital.

Cautious Optimism

- Roundtable President and CEO Jeffrey DeBoer said, “Our current Sentiment Index shows improved optimism by industry leaders, compared with previous surveys that highlighted significant market concerns. The Q1 sentiment continues to note challenges presented by ongoing tight capital markets, increased operating expenses, and the continuing uncertainty of post-pandemic, in-office work. However, as the interest rate environment appears to have settled somewhat, executives are now expressing increased optimism that values and capital availability will improve in 2024.”

- He added, “As we look at the current and future landscape of commercial real estate, it’s clear that we are at a pivotal moment. With nearly $3 trillion of commercial real estate loans maturing in the next four years, it remains very crucial that lenders continue to work constructively with borrowers to reflect both current and expected economic growth. Markets and asset values continue to adjust and stabilize as office use, interest rates, and inflation begin to normalize.”

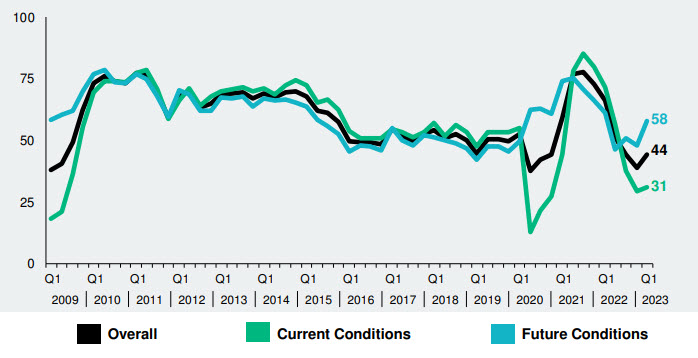

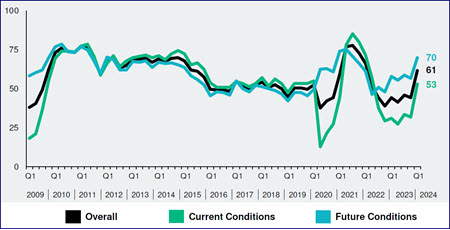

- All indices of The Roundtable’s Q1 Index are up, compared to the previous quarter and one year ago. The Index—a measure of senior executives’ confidence and expectations about the commercial real estate market environment—is scored on a scale of 1 to 100 by averaging the scores of Current and Future Economic Sentiment Indices. Any score over 50 is viewed as positive.

Topline Findings

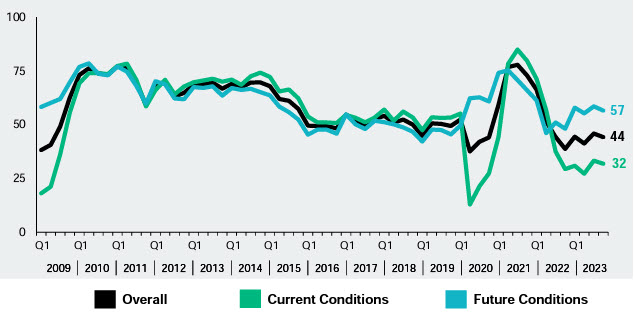

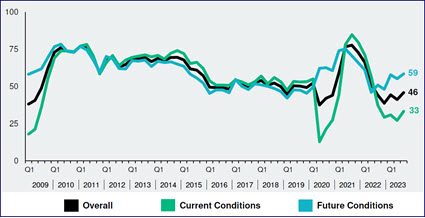

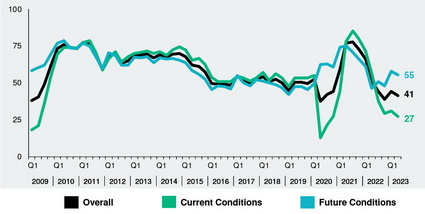

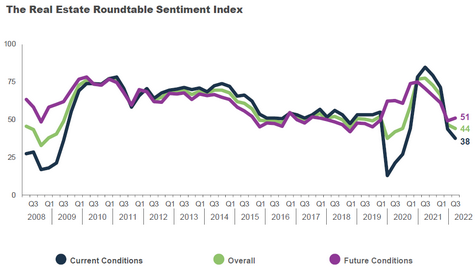

- The Q1 2024 Real Estate Roundtable Sentiment Index registered an overall score of 61, an increase of 17 points from the previous quarter. The Current Index registered 53, a 21-point increase over Q4 2023, and the Future Index posted a score of 70 points, an increase of 13 points from the previous quarter. These increases point to cautious optimism in the real estate market.

- There continue to be variations among asset classes and within specific property types as the real estate market rapidly changes. Industrial and multifamily are starting to soften, but retail and hospitality asset classes were identified as being surprisingly resilient. While many office properties have experienced a significant erosion in value, Class A offices continue to outperform.

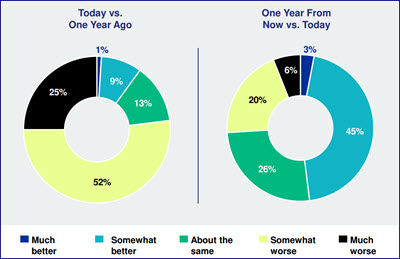

- An overwhelming 79% of survey participants indicate that asset values have decreased compared to the previous year. However, the potential end to interest rate hikes has instilled some industry optimism, with nearly 80% of survey participants expecting asset values to be the same or higher a year from now.

- Survey participants continue to emphasize the challenging capital markets landscape, with 86% and 85% of survey participants suggesting that the availability of equity and debt capital, respectively, is the same or worse than a year ago. That said, 67% and 76% believe the availability of equity and debt capital, respectively, will improve a year from now.

Data for the Q1 survey was gathered in January. See the full Q1 report.

# # #