President Donald Trump on Wednesday said he would move to ban “large institutional investors” from purchasing single-family homes, framing the proposal as part of a broader push to improve housing affordability. (Washington Post | CNBC, Jan. 7)

State of Play

- “I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it. People live in homes, not corporations,” Trump wrote in a post on Truth Social. (Bloomberg, Jan. 8)

- He indicated plans to discuss the issue at the World Economic Forum in Davos, Switzerland, later this month. (WSJ, Jan. 7)

- The White House did not specify what executive actions, if any, would be taken, nor how it would define “large institutional investors.”

- As currently described, the proposal would apply only to future acquisitions and would not require existing owners to divest their single-family rental (SFR) portfolios. (GlobeSt., Jan. 8)

- Codifying a ban would require clear statutory language passed by Congress and signed into law—raising complex questions around thresholds, exemptions, and enforcement.

- Legal challenges would likely follow, including claims related to takings, equal protection, and interstate commerce. Absent congressional authorization, the executive branch lacks clear authority to impose such a restriction solely through regulation. (Propmodo, Jan. 8)

- Former House Financial Services Committee Chair Patrick McHenry said on Bloomberg on Thursday that housing affordability challenges are driven largely by state and local land-use and regulatory barriers, noting that institutional investors account for only a small share of the housing market. (Bloomberg, Jan. 8)

- Also this week, Trump wrote on Truth Social that he is directing Fannie Mae and Freddie Mac to purchase $200 billion in mortgage bonds to address the national housing affordability crisis. Federal Housing Finance Director Bill Pulte said in an interview that Fannie and Freddie Mac will carry out the president’s directive by purchasing $200 billion in mortgage-backed securities from the public market. (Politico | Bloomberg, Jan. 9)

What the Data Shows

- Research consistently finds that housing affordability pressures stem primarily from chronic supply shortages, high construction costs, and elevated mortgage rates—not institutional ownership levels.

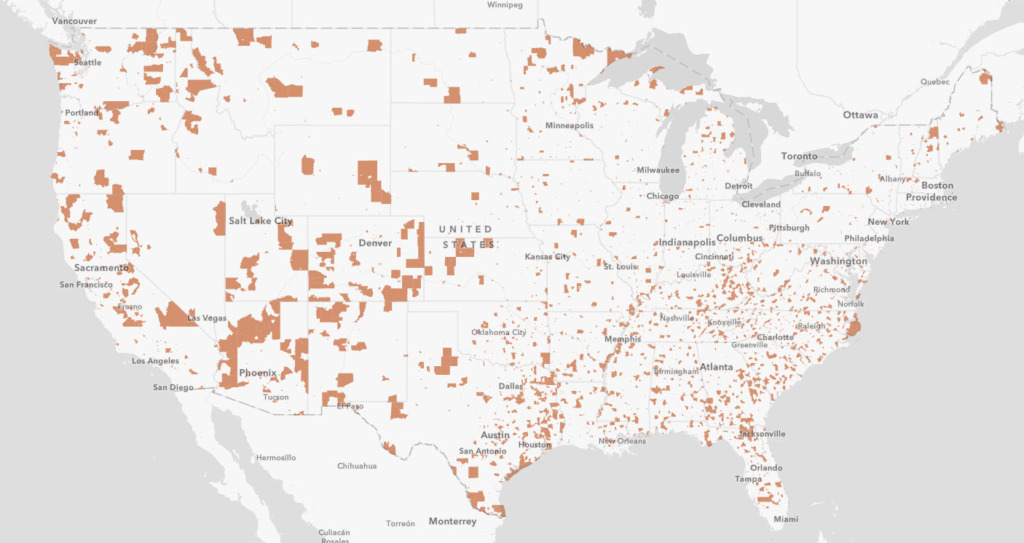

- According to SFR Analytics, the top 24 SFR owners control just over 520,000 homes—about 3.5% of rental homes and less than 1% of the total single-family housing stock—underscoring the limited market impact of large investors. (Bloomberg, Jan. 7)

- Single-family rentals expanded after the Great Financial Crisis in 2008-2009 as investors helped absorb foreclosures, stabilize neighborhoods, and provide rental housing for households unable to buy. (Federal Reserve Bank of St. Louis, Oct. 2025)

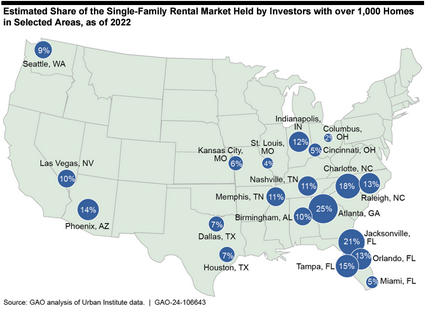

- A 2024 Government Accountability Office (GAO) report found that large institutional investment expanded rental-housing options, helped stabilize neighborhoods after the financial crisis, and improved access to quality communities for low- and middle-income households. (GAO Report Highlights | Full GAO Report) (Roundtable Weekly, June 2024)

- The GAO study also found that large-scale SFR showed that many working families desire the space provided by single-family homes, but may have low credit scores and otherwise can’t afford to buy them. Renting is commonly their best option for moving into better neighborhoods and school districts.

- Another study out of UNC Charlotte, released in May 2024, finds that children from low- and moderate-income households see improved achievements in school when they rent single-family homes in neighborhoods where they cannot afford to buy. (UNC Study Highlights | Full UNC Report, 2024)

- Research published by the Brookings Institution and the Urban Institute estimates that large institutional investors own only 3 percent of the single-family home rental stock, and that percentage drops to about 1.5 percent of rental stock if townhomes, duplexes, and apartments are also included. (Brookings Institution Report, 2023; Urban Institute Report, 2023)

- An August 2025 report from the American Enterprise Institute found that institutional investors are not a primary driver of housing unaffordability, noting that housing shortages stem largely from restrictive zoning, limited new construction, and inflationary pressures. (American Enterprise Institute Report, Aug. 2025)

- Stephen Scherr, co-president of Pretium Partners, which owns Progress Residential (RER member) one of the nation’s largest SFR operators, said on CNBC today that institutional investors help expand housing supply by de-risking large developments through purchase commitments that enable projects to move forward. He added that many renters they serve are not mortgage-eligible and use renting as a pathway to eventual homeownership. (CNBC, Jan. 9)

Roundtable View

- Expanding the supply of housing across the geographic and economic spectrum is essential for the nation’s economic vitality.

- Large-scale SFR investments have helped revitalize distressed properties and communities, contributing to economic growth and stability.

- The Real Estate Roundtable (RER) has consistently emphasized that restricting capital will not solve the affordability crisis, and that increasing housing supply is the most effective path forward.

- RER President and CEO Jeffrey DeBoer said: “Access to affordable housing is central to the American Dream, a dream that for some families means renting a home and for others means owning a home. For more than a decade, our nation’s supply of both owner-occupied and rental housing has, for a variety of reasons, not kept up with demand. This gap between supply and demand is the true cause of today’s housing crisis. The supply of housing must be increased.”

- “This will require, among other actions, common sense policy reforms to local permitting and zoning regulations, recognizing in both national and local policy actions the reality of escalating labor and material costs and, importantly, the need to maintain and improve incentives to encourage the capital needed to develop, redevelop, and modernize the nation’s housing stock,” DeBoer said. “We work with all policymakers to advance initiatives that remove barriers to housing development, incentivize capital investment in housing, and help people achieve the American Dream.”

- In March 2025, RER and Nareit submitted comments to the Federal Trade Commission (FTC) in response to the agency’s inquiry into the impact of large-scale SFR operators and institutional investors on home prices and rents. (Letter, March 2025)

- The letter emphasized that institutional investors account for a small fraction of home purchases and play a limited, but constructive role in expanding supply, rather than driving affordability challenges. (Roundtable Weekly, March 2025)

- This week, RER member Sean Dobson (Chairman, CEO & CIO, Amherst) said restricting investment would not improve affordability. “Banning investors from putting capital into the housing market is not going to make affordability any better,” Dobson said during an appearance on Wednesday on Bloomberg Markets. (Bloomberg, Jan. 7)

Without meaningful steps to expand housing supply, proposals to limit institutional participation are unlikely to address the root causes of affordability pressures facing renters and would-be homebuyers, reinforcing RER’s ongoing work with policymakers and the administration to promote policies that increase housing supply and improve affordability.