Negotiations between Democrats and Republicans over the next round of COVID-19 relief stalled this week after policymakers could not bridge significant differences between the GOP’s $1 trillion package released Monday and the $3.4 trillion proposal House Democrats passed in May. (BGov, July 30 and Roundtable Weekly, May 22)

- “We’re still very far apart on a lot of issues,” Treasury Secretary Steven Mnuchin said on July 29 after three days of meetings with House Speaker Nancy Pelosi (D-CA), Senate Minority Leader Charles Schumer (D-NY) and White House Chief of Staff Mark Meadows. “I do think there is a subset of issues that we do agree on, but overall we’re far from an agreement.” (RollCall, July 29)

- Mnuchin added that negotiating a compromise on unemployment insurance, state and local government assistance, and liability protections for businesses are especially challenging. “It makes it the pending business for next week,” said Majority Leader Mitch McConnell (R-KY) [CQ, July 29].

- CARES Act benefits regarding $600 weekly unemployment insurance and the federal residential tenant eviction moratorium expire today – placing additional pressure on lawmakers to reach agreement before the congressional recess, scheduled to start on August 8.

HEALS Act Provisions

- Senate Republicans on July 27 unveiled the “Health, Economic Assistance, Liability Protection, and Schools (HEALS) Act.” The GOP package would reduce the expanded unemployment benefit to $200 per week, authorize another round of $1,200 stimulus checks to most Americans, provide more than $100 billion for reopening schools, among other provisions. (Appropriations Committee news release, July 27 and Republican Policy Committee summary, July 28)

- The GOP’s HEALS Act is comprised of eight bills that form a base for negotiations with Democrats, who passed the $3.4 trillion “Health and Economic Recovery Omnibus Emergency Solutions Act [HEROES] Act” (H.R. 6800) in the House in May. (How the HEALS Act compares to the HEROES Act, CNBC, July 30 and HEALS Act Comparison to HEROES Act and Current Law, Brownstein Hyatt Farber Schreck, July 31)

The HEALS Act includes:

- Liability protections in the “Safeguarding America’s Frontline Employees To Offer Work Opportunities Required to Kickstart the Economy (SAFE TO WORK) Act,” introduced by Sens. John Cornyn (R-TX) and Mitch McConnell (R-KY). A billsummary notes it would “create a federal cause of action for coronavirus exposure claims” that preempts state laws outside of workers’ compensation regimes. A business defendant would lose the liability shield if it engaged in “gross negligence” or “willful misconduct” in causing the plaintiff’s COVID-related injuries. (Summary of the Act)

The Real Estate Roundtable joined approximately 480 business groups in a July 30 letter urging Congress to support the liability relief provisions. (The Hill, July 30)

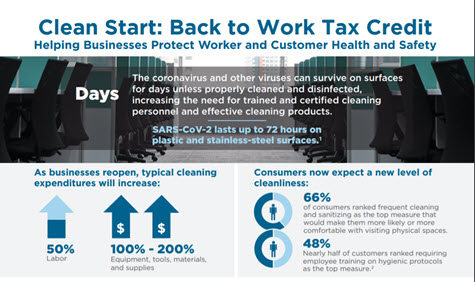

- The Safe and Healthy Workplaces Tax Credit in the “American Workers, Families and Employers Assistance Act” introduced by Senate Finance Committee Chairman Charles Grassley (R-IA). [Section-by-section summary] The proposal would provide a refundable payroll tax credit for 50% of the costs associated with protecting employees (testing, PPE, cleaning, etc.), reconfiguring workplaces, and upgrading workplace technology to prevent the spread of COVID-19. Expenses between March 13 and the end of this year would qualify, and the maximum credit would be based on the number of employees. The measure reflects stand-alone legislation recently introduced by Senator Rob Portman (R-OH) and Rep. Tom Rice (R-SC). [Roundtable Weekly, July 24]

- A Wall Street Journal video released yesterday profiles the extensive efforts of commercial real estate companies to accommodate the safe return of workers to offices, featuring Roundtable member Scott Rechler (Chairman and Chief Executive Officer, RXR). The video features the use of new technological tools, revised layout plans and enhanced ventilation systems to enhance the well-being of building occupants.

- A second round of funding for the Paycheck Protection Program (PPP) would be provided in the “Continuing Small Business Recovery and Paycheck Protection Program Act,” introduced by Sens. Marco Rubio (R-FL) and Susan Collins (R-ME). The $190 billion bill would fund PPP “second draw” loans; a new Section 7(a) loan program for Recovery Sector Businesses; and numerous program criteria reforms. (Section-by-section summary and one-pager.)

- In other pandemic relief news, a bill introduced on July 29 by members of the House Committee on Financial Services, Van Taylor (R-TX), Al Lawson (D-FL), and Andy Barr (R-KY), would provide economic support to the commercial real estate market, especially for businesses with Commercial Mortgage-Backed Securities (CMBS) debt. The “Helping Open Properties Endeavor (HOPE) Act” (H.R. 7809) would establish a Treasury facility to encourage bank loans in the form of preferred equity to help struggling CMBS borrowers. (Wall Street Journal and Rep. Taylor news release, July 29)

- Federal Reserve Chairman Jay Powell on July 29 held a news conference after a two-day meeting of the Federal Open Market Committee (FOMC) to address interest rates and the repercussions of the pandemic. Powell stated, “To support the flow of credit to households and businesses, over the coming months the Federal Reserve will increase its holdings of Treasury securities and agency residential and commercial mortgage-backed securities at least at the current pace to sustain smooth market functioning.” (FOMC statement and new conference video, July 29)

As pandemic negotiations continue in Congress, The Roundtable and its real estate industry partners remain engaged in issues of vital importance to CRE. See the story below for more details presented this week in a webinar held by Walker & Dunlop.

# # #