As focus on Capitol Hill shifted to appropriations talks this week, The Real Estate Roundtable (RER) and a broad coalition of organizations representing the real estate, consumer products, manufacturing, and retail sectors sent a letter urging congressional leaders to ensure that the ENERGY STAR program remains amply funded in the 2027 fiscal year (FY’27), starting Oct. 1.

Coalition Advocacy

- On Tuesday, the multi-industry coalition requested that House and Senate appropriators include explicit funding for ENERGY STAR in the FY’27 spending bill, in line with FY’26 funding levels. (Letter, April 14)

- The letter also encouraged lawmakers to include strong congressional oversight measures in the legislation, as lead agency responsibilities for the program shift from the Environmental Protection Agency (EPA) to the Department of Energy (DOE). (Letter, April 14)

- In the letter, the coalition recommended that legislators consolidate past funding for ENERGY STAR expressly given to the EPA, plus amounts used by DOE historically to run its portion of the program. (Letter, April 14)

- Congress provided approximately $33 million for ENERGY STAR to EPA in the FY’26 appropriations bill (H.R. 6938), signed into law on Jan. 23, preserving the program through Sept. 30 following earlier reports that it could be privatized or defunded. (Roundtable Weekly, April 3)

- Though President Trump’s FY’27 budget request, released this month, does not specifically mention ENERGY STAR—as was the case last year—the White House has proposed cutting DOE and EPA’s overall budgets by 11 percent and 52 percent, respectively. (Budget of the U.S. Government, April 3)

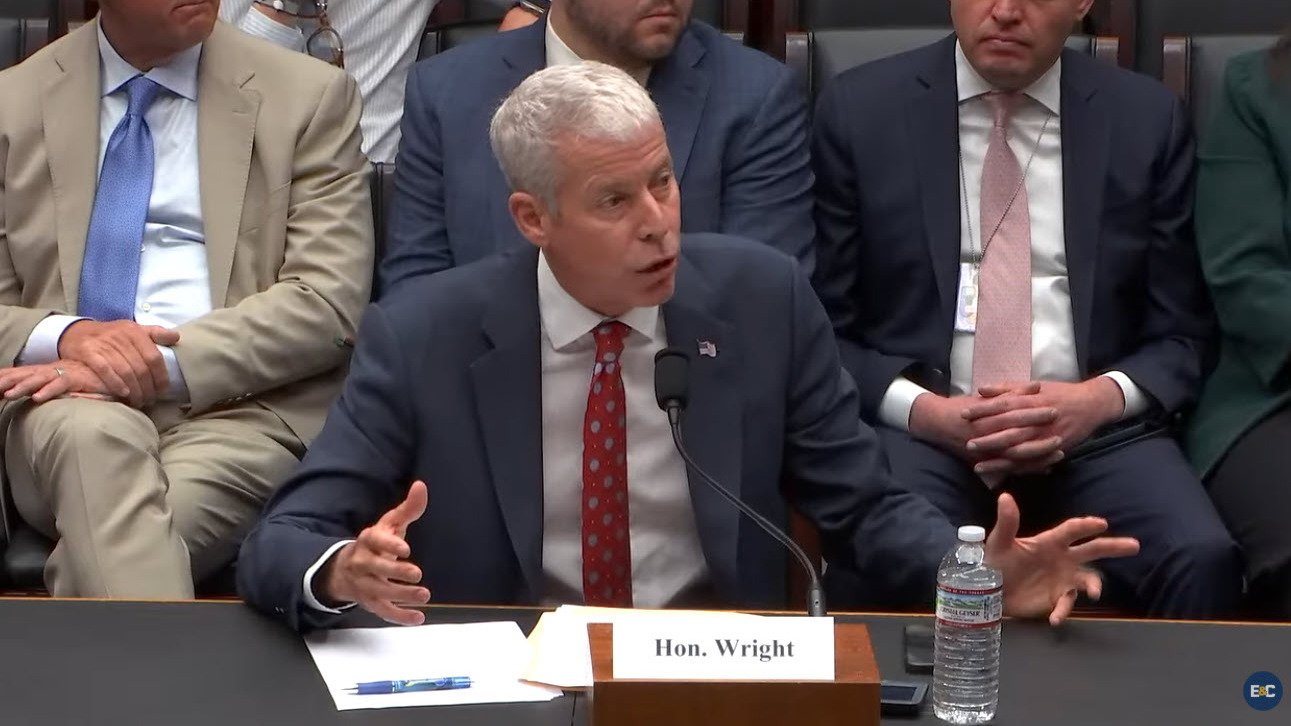

DOE Budget Hearings

- This week, DOE Secretary Chris Wright appeared before the House Committee on Energy and Commerce (E&C) and a subcommittee of the House Committee on Appropriations to discuss the agency’s FY’27 budget request.

- Though most of Sec. Wright’s testimony did not focus on ENERGY STAR, Rep. Paul Tonko (D-NY) raised the topic during Thursday’s E&C hearing. (Watch Hearing)

- Rep. Tonko noted the importance of ENERGY STAR and pointed out that ENERGY STAR has historically required approximately $35 million in annual funding. (Watch Hearing)

- When asked if DOE would be seeking that funding as part of its budget request, and if he could provide assurance that DOE is already working to put the people and resources in place to transition and manage the program, Sec. Wright said he would follow up on the details. (Watch Hearing)

- Still, Sec. Wright added that he is “all for” voluntary energy efficiency ratings on appliances as well as data and transparency. (Watch Hearing)

- The bulk of the two hearings this week focused on a range of other topics, including rising energy prices, permitting reform, and nuclear power. (Politico E&E News, April 16)

Roundtable View

- In March, RER and coalition partners sent a letter expressing support for DOE assuming its new role as lead federal agency for ENERGY STAR. (Roundtable Weekly, April 3)

- Additionally, the March letter underscored that DOE is well-positioned to lead a modernized program that continues to provide consumers and businesses with access to efficient products and buildings that uphold the performance they have come to expect from the ENERGY STAR brand. (Roundtable Weekly, April 3)

- RER and coalition partners have long made the business case for ENERGY STAR and emphasized its status as a federal program required by law—meaning that it cannot be privatized or operated outside the U.S. government by agency decree. (Roundtable Weekly, April 3 | Roundtable Weekly, March 6)

- As Tuesday’s coalition letter highlighted, “Since 1992, ENERGY STAR and its partners have helped American families and businesses save more than $500 billion in energy costs.” (Letter, April 14)

- By driving cost savings through energy efficiency, the program contributes to reducing energy waste and freeing up capacity on the electricity grid, in alignment with President Trump’s goal to “unleash America’s energy dominance.” (RER Policy Priorities Document)

Next week, Sec. Wright is scheduled to appear before Senate appropriators to discuss DOE’s budget request. RER will continue to track developments related to ENERGY STAR funding and support the continuation of the program and its smooth transition to DOE.