House leaders this week released amended text of the Senate-passed 21st Century ROAD to Housing Act, preserving major pro-housing provisions aimed at increasing supply, improving affordability, and expanding housing options across the country. The revised package is expected to receive a House vote next week, before returning to the Senate for final approval. (Politico | Bisnow | The Hill, May 14)

State of Play

- House Republican leaders continued reworking the Senate-passed 21st Century ROAD to Housing Act this week, even as President Donald Trump publicly urged Congress to pass the Senate bill as written. (Politico, May 11)

- Speaker Mike Johnson (R-LA) said Friday that he still intends for the House to vote on changes to the Senate’s housing package, despite opposition from White House officials and Senate Republicans. “We’re focused on producing a housing bill that meets all the objectives,” Speaker Johnson said. “It’ll be bipartisan, bicameral.” (Politico, May 15)

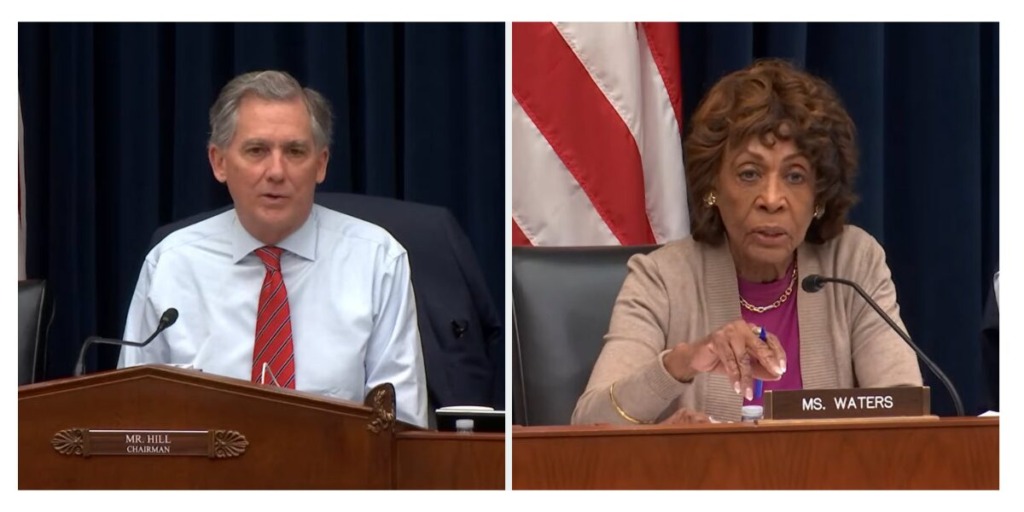

- House Financial Services Committee Chairman French Hill (R-AR) and Ranking Member Maxine Waters (D-CA) released the House’s amended text Thursday, with leadership aiming to bring the bill to the floor next week. (The Hill, May 14)

- Rep. Hill said the bipartisan amendment reflects concerns raised by members and stakeholders, adding that it “cuts unnecessary barriers to new home construction, modernizes Department of Housing and Urban Development (HUD) programs, and allows banks to more freely deploy funding into their communities.” (Rep. Hill Statement, May 14)

- Speaking to reporters Friday, Rep. Hill said the House bill addresses legal concerns raised by the Senate’s investor restriction language, including its forced-sale requirement for certain build-to-rent homes. “It’s in the bill in the right way. I think it removes some of the legal challenges that we felt that were in the structure of the Senate bill. We think this has made a better bill.” (Politico, May 15)

- Rep. Waters said the updated bill “restores key provisions to hold institutional investors accountable and protect renters, while expanding access to affordable housing opportunities for families across the country.” (Rep. Waters Statement, May 15)

- In a statement following the release, RER said the amended bill makes significant improvements by removing the forced-disposition requirement that would have raised serious constitutional concerns, chilled investment in new rental housing, prevented the construction of thousands of homes, and worsened supply constraints in markets across the country. (RER Statement, May 14)

- Progressive and conservative groups alike have cited numerous benefits that single-family rental (SFR) owners and builders deliver to U.S. housing markets, including increasing supply, maintaining and improving homes, and providing opportunities for families to live in communities with strong education systems where homeownership may be out of reach. (Progressive Policy Institute | Competitive Enterprise Institute, February 2026) (Roundtable Weekly, April 17 | April 10)

Key House Revisions

- The package includes broad housing supply and affordability reforms to reduce barriers to new construction, support manufactured housing innovation, streamline environmental reviews, and modernize HUD programs.

- The updated House text removes the Senate bill’s forced-disposition requirement for build-to-rent housing, while retaining restrictions and enforcement provisions related to future single-family home acquisitions by large institutional investors. (The Hill, May 14)

- Additionally, it would create grant programs for converting abandoned buildings into housing, expand community lending, and strengthen tools to encourage local zoning and pro-housing policies.

Roundtable Advocacy

- RER and broad housing coalitions have consistently emphasized that housing affordability is driven by supply shortages, construction costs, and mortgage rates—not institutional ownership levels—and that restricting institutional capital would only make it harder to meet the nation’s growing housing needs. (Roundtable Weekly, Jan. 9 | Jan. 16 | Jan. 23 | Feb. 27| March 6 | March 13 | March 20 | March 27 | April 3 | April 10 | April 17 | April 24 | May 1 | May 8)

- RER called on Congress this week to remove the forced-sale provision, citing a white paper by former U.S. Solicitor General Paul Clement warning that the provision raised serious constitutional concerns. (RER Letter, May 12 | Roundtable Weekly, April 17)

- Following the release of the amended text, RER and a broad housing coalition urged Congress to pass the bill quickly, calling it a major opportunity to expand supply, improve affordability, and broaden housing choice. (Coalition Letter | Coalition Statement | May 14)

- The housing crisis cannot be solved without building more affordable homes of every type, in every market and for every stage of life — including rental housing, workforce housing and paths to homeownership,” said RER President & CEO Jeffrey DeBoer. “Restricting capital will only make that shortage worse. Increasing supply is the path forward.” (RER Statement | May 14)

HUD Raises Concerns

- HUD Secretary Scott Turner wrote to congressional leaders Friday to remove parts of the House-amended bill related to institutional investor restrictions and a new tenant hotline, warning they could create significant operational challenges for HUD and expand the department’s role in state and local housing matters. (PoliticoPro, May 15)

- Sec. Turner also testified before House and Senate appropriators this week on the administration’s fiscal 2027 HUD budget request, emphasizing the need to reduce regulatory barriers, streamline permitting, and lower housing production costs. (Politico, May 12)

- Sec. Turner cited local zoning restrictions, environmental reviews, and federal regulations as major drivers of housing costs, while lawmakers in both parties raised concerns about proposed HUD funding cuts. (House Appropriations Subcommittee Hearing, May 12)

- Lawmakers also highlighted Opportunity Zones (OZs) and public-private partnerships as housing production tools. Sec. Turner defended OZs as “very transformative,” saying public-private partnerships are “crucial and key” to increasing affordable housing supply and revitalizing communities. (Senate Appropriations Subcommittee Hearing, May 14)

RER and its coalition partners appreciate the bipartisan work of House and Senate leaders and urge swift passage of the housing bill to expand access to homeownership and rental housing opportunities nationwide.