The House Ways and Means Committee this week passed a comprehensive tax package that preserves critical features of current law while extending and improving real estate provisions supported by The Real Estate Roundtable. However, the legislation encountered a substantial setback Friday morning, when the House Budget Committee rejected the “One Big Beautiful Bill,” which combined the work of the Ways and Means and other House committees. (Axios, May 16)

“Taken as a whole, the tax proposals in the Chairman’s amendment will spur needed investment in our nation’s housing supply, strengthen urban and rural communities, and grow the broader economy to the benefit of all Americans,” said Roundtable President and CEO Jeffrey DeBoer. (Read DeBoer’s full statement here)

State of Play

- The House Budget Committee rejected the bill in a 16-21 vote after GOP leadership failed to secure sufficient support from several Republican holdouts. (Axios, May 16)

- President Trump on Friday urged Republicans to fall in line and support the massive reconciliation package amid sparring among members on the Hill over various provisions. “Republicans MUST UNITE behind, ‘THE ONE, BIG BEAUTIFUL BILL!’” Trump posted on Truth Social.

- House GOP leaders plan to continue private talks with the reluctant Republicans and the White House over the weekend in hopes of resurrecting the package next week. (Politico, May 16)

What’s In and Out for CRE

- As currently drafted, the House legislation maintains the full deductibility of state and local business-related property taxes.

- Carried interest, capital gains, like-kind exchanges, and general cost recovery periods for commercial real estate would remain unchanged.

- Section 199A Deduction Boost: The legislation permanently increases the pass-through business income deduction from 20% to 23%, preserving eligibility for REIT dividends and effectively lowering the maximum tax rate on qualifying income to 28.49%.

- 100% Bonus Depreciation: The Ways and Means Committee is proposing to reinstate 100% bonus depreciation for five years (2025–2030), incentivizing investments and upgrades in nonresidential properties.

- Opportunity Zones: The legislation extends the Opportunity Zone tax incentives through 2033 and would set aside 33% of new OZ designations for rural areas.

- Low-Income Housing Tax Credit: The legislation increases the allocation of low-income housing credits by 12.5% for four years and permanently reduces the threshold of private activity bond financing necessary for projects to otherwise qualify for credits.

- Energy Tax Incentives: The Ways and Means legislation repeals or phases out tax incentives such as the section 48 tax credit for solar panel and other clean energy investments, the 45L tax credit for new home construction, and the section 30C tax credit for EV recharging stations. (See more in Energy story below)

- Factory Expensing: Other tax changes would temporarily allow newly constructed manufacturing, agricultural and refining properties to qualify for 100% expensing.

Roundtable Advocacy

- RER President and CEO Jeffrey DeBoer provided insights on these developments during a fireside chat at the ULI Spring Meeting in Denver this week. DeBoer discussed the current political climate, policy implications for commercial real estate, and outlined both emerging risks and opportunities shaping the industry’s future.

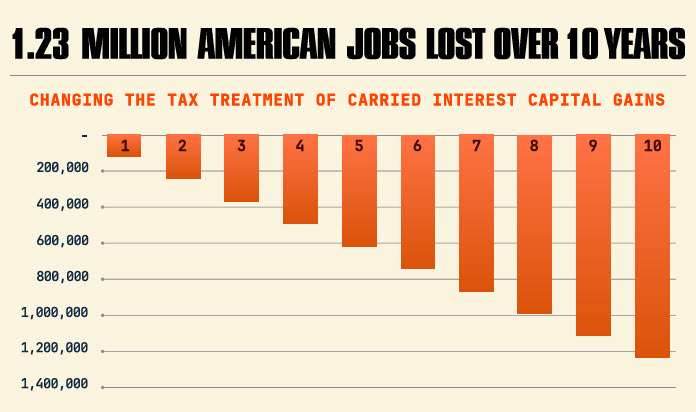

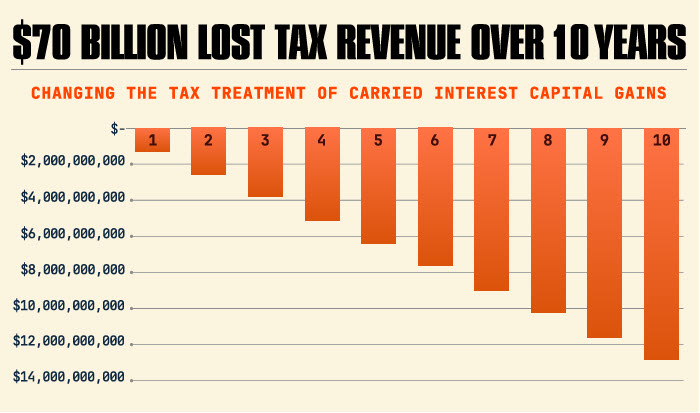

- With the President advocating for changes to carried interest taxation, RER urges its members to continue contacting lawmakers to express strong support for preserving current law (RER’s Tax Talking Points | Hot Button Items | Tax Policy Priorities) (Contact Members of Congress) (GlobeSt., May 16)

Housing News

- The Ways and Means Committee’s provisions to expand the Low-Income Housing Tax Credit (LIHTC) align with components of the Affordable Housing Credit Improvement Act (AHCIA). (Affordable Housing Finance, May 16) (RW, May 2)

- The House Financial Services Subcommittee on Housing and Insurance held a hearing this week titled, “Expanding Choice and Increasing Supply: Housing Innovation in America,” focused on how modern construction technologies could increase moderate-income housing supply while identifying regulatory and financing barriers that limit broader adoption.

- Lawmakers and witnesses explored alternative housing solutions such as manufactured housing, modular construction, and 3-D printed homes as ways to help close the housing supply gap. (Watch Hearing, May 14)

Looking Ahead

- House Ways and Means Chair Jason Smith (R-MO) expressed interest in passing a separate bipartisan tax package by the end of the year, at an appearance at the Economic Club of Washington, D.C. earlier this week. This package would include expiring tax provisions and healthcare-related items.

- “I would love to work with Sen. Wyden, Chairman Crapo, ranking member Neal in trying to craft a bipartisan bill before the end of the year, because there’s a lot of tax provisions that I really care about that are expiring, or have expired, that are truly, truly bipartisan,” said Smith. (PoliticoPro, May 15)

- Senate Finance Committee Chair Mike Crapo (R-ID) and fellow panel member Sen. Steve Daines (R-MT) are pushing to extend business tax cuts beyond the expiration set by Ways and Means, the latest change the Senate wants to make to the bill. (Reuters, May 16)

With the Budget Committee setback, the immediate future of the tax package is uncertain. But the provisions are certain to change further as the debate shifts to the Senate.