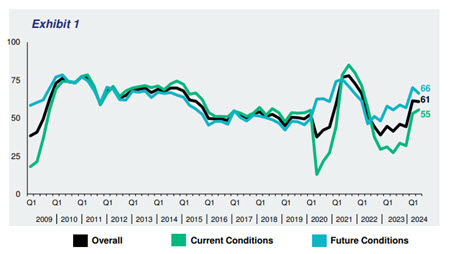

(WASHINGTON, D.C.) — The Real Estate Roundtable (RER) today released its Q2 2025 Sentiment Index, reporting a decrease in confidence in the commercial real estate market environment among industry executives due to policy uncertainty, rising costs, and cautious investor sentiment. The quarterly Sentiment Index, measuring executive perceptions on market conditions, asset values, and capital availability, declined to an overall score of 54, down 14 points from last quarter. The Current Conditions Index dropped to 50, reflecting a 15-point decline, while the Future Conditions Index decreased by 12 points, settling at 58. The Overall Index is scored on a scale of 1 to 100 by averaging Current and Future Indices; any score over 50 is viewed as positive.

RER President and CEO Jeffrey DeBoer said, “While respondents note early signs of market stabilization and improved transactional discipline, lingering concerns over U.S. trade policies and other economic headwinds are tempering optimism for the remainder of 2025. The office sector remains under pressure, but is experiencing a gradual rebound as return-to-office trends continue to shift closer to pre-pandemic patterns.”

He added, “Uncertain tariff policies are driving up construction costs and weighing on long-term investment decisions. At the same time, the Federal Reserve’s decision to hold interest rates steady is slowing capital formation and delaying needed transactions. We need pro-growth economic policies that encourage productive investment, strengthen communities, and promote long-term stability. Extending and making the2017 Tax Cuts and Jobs Act (TCJA) provisions permanent, along with advancing incentives to address our nation’s housing supply shortage, are crucial to help achieve these goals.”

The Q2 Sentiment Index topline findings include:

- The Q2 2025 Real Estate Roundtable Sentiment Index registered an overall score of 54, a decrease of 14 points from the previous quarter. The Current Index registered at 50, a 15-point decrease compared to Q1 2025. The Future Index posted a score of 58 points, a decrease of 12 points from the previous quarter, reflecting uncertainty around policy direction, rising costs, and execution risk. While market sentiment remains cautious, respondents are seeing early signs of stabilization and improved transactional discipline. Nevertheless, expectations for improvement have softened compared to last year, and many investors remain hesitant to re-engage.

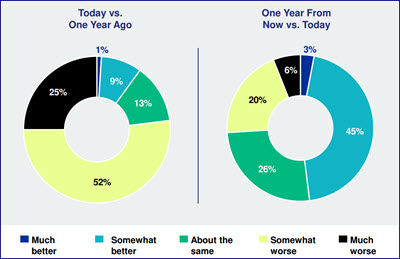

- Market conditions remain mixed, with general uncertainty, along with sector and geographic bifurcation, driving sentiment. 37% of respondents believe that general market conditions are worse than this time last year, and 37% of respondents believe that general market conditions are better than this time last year. Close to half (47%) of Q2 survey participants expect general market conditions to show improvement one year from now, while 20% of Q2 participants expect general market conditions to be somewhat worse in a year. Logistics and high-quality multifamily remain bright spots, while hospitality and office—particularly commodity space—continue to face significant challenges. From a geographic standpoint, the Midwest is showing relative resilience, whereas sentiment around the Sunbelt reflects concern over elevated supply and near-term softened demand.

- 42% of respondents believe asset values are roughly unchanged compared to a year ago. The remaining respondents are divided, with 22% believing asset prices have increased and 36% believing they have declined. Looking ahead, the outlook is cautious: 38% expect asset prices to remain stable over the next year, while another 38% anticipate a slight decline.

- Perceptions of equity capital are widely varied, though 34% of respondents believe the availability of equity capital is better than it was a year ago. Sentiment around debt capital has brightened, as 43% said the availability of debt capital has improved from last year. Looking forward, 45% of respondents believe that equity capital availability will be better in one year and 39% believe debt capital availability will be better in one year.

Some sample responses from participants in the Sentiment Index’s Q2 survey include:

“The one thing that every investor – domestic and foreign – wants is stability. The environment in the United States is incredibly unstable, so some of our investors are sitting on the sidelines.”

“Foreign capital flows into the U.S. will shrink in the near term. That said, the U.S. is typically the first market to readjust in terms of pricing, and that will create opportunity.”

“We’re starting to see slightly more trades, which opens up the door to better visibility into valuations, and as a result, may improve the comfort and volume of future trades.”

Data for the Q2 survey was gathered by Chicago-based Ferguson Partners on RER’s behalf in April. See the full Q2 report.

The Real Estate Roundtable brings together leaders of the nation’s top publicly-held and privately-owned real estate ownership, development, lending and management firms with the leaders of major national real estate trade associations to jointly address key national policy issues relating to real estate and the overall economy.

# # #